Enrico Turrin is the deputy director of the European Publishers Federation and has been providing Readmagine’s audience with his insider’s insight into the evolution of the book markets for many years. In this edition of Readmagine, the title of the Kraftwerk song «Transeurope Express» was chosen as the title of his presentation.

This video features Turrin’s entire presentation, complete with charts and data tables. Below is a summary of his presentation, structured by topic.

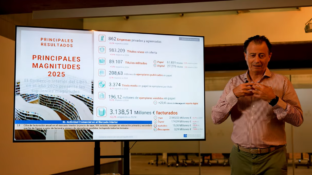

The European book market, as presented by the European Federation of Publishers, continues to demonstrate resilience and growth, albeit with notable fluctuations influenced by various economic and social factors. In 2024, the net publisher’s turnover reached nearly €25 billion annually, marking a consistent increase for the third consecutive year. This growth trend contrasts with a peak turnover of €24.5 billion in 2007, just before the financial crisis, indicating a recovery and surpassing of previous levels.

Impact of COVID-19 and economic factors

The COVID-19 pandemic, while disruptive, surprisingly buoyed the market in 2021 with the largest single-year increase in over two decades. This surge can be attributed to increased reading habits as alternative leisure activities like cinemas and concerts were restricted. However, subsequent years have shown a stabilization rather than continued rapid growth, with overall turnover increasing slightly due to price inflation rather than volume.

Inflation and real market value

An important consideration is the impact of inflation on nominal turnover figures. Over the past 20 years, while nominal turnover has increased, the real market value has declined by approximately 30%, highlighting the need for a nuanced understanding beyond nominal figures. This discrepancy underscores challenges in accurately assessing market health solely through nominal values.

Market size and consumer spending

The market size, encompassing net turnover plus discounts and taxes, approaches €40 billion when accounting for consumer spending within the European Union. This figure illustrates the significant economic contribution of the publishing sector to cultural diversity and educational resources across the continent.

Publishing trends and titles

Annually, approximately 585,000 new titles are published in Europe, reflecting a complex interplay of market dynamics. Despite variations across countries, the sector continues to contribute substantially to cultural diversity, with over 14 million titles available for sale in various formats, including digital and audio.

Sector composition and distribution channels

The sector’s composition is diverse, with children’s books showing resilience, while trade books dominate with over 51% market share. Distribution channels have witnessed notable shifts, with online sales gaining ground during the pandemic, accounting for nearly 30% of total sales by 2023.

Formats and digital transformation

Print remains the preferred format, contributing over 80% of total turnover, despite significant digital advancements in certain genres like academic and genre fiction. The digital segment, however, is underrepresented due to challenges in capturing sales data from major digital platforms like Amazon and self-publishing avenues.

Emerging trends: audiobooks and international markets

Audiobooks have emerged as a rapidly growing segment, though their exact market share remains underestimated due to subscription models and digital distribution complexities. Internationally, export markets, particularly within Europe and to Latin America, continue to play a crucial role in sector expansion.

Online book purchases and e-commerce growth

In 2024, 15% of the European population is estimated to buy books and publications, including newspapers, magazines, and both print and digital books, online. Notably, Ireland stands out with more than 25% of its population purchasing books online, possibly due to significant cross-border book purchases from the UK. This trend reflects the growing influence of e-commerce on the book market across Europe. Additionally, there is a marked difference in the level of digital adoption among European countries, with the Nordic countries, the Netherlands, and Ireland displaying higher levels of online book purchases compared to other regions.

Reading habits: a concerning trend in Europe

Eurostat’s long-awaited survey on reading, based on 2022 data, highlights an alarming trend: 55% of men in Europe do not read books, a figure that raises concerns about the cultural and social health of European societies. Conversely, the figure is lower for women, with 40% not engaging in reading. This gap between genders is worrying and may suggest that men, in particular, have room to improve their reading habits. However, the results are not without criticism, as the methodology has been questioned, particularly the exclusion of younger children (who read a significant number of books). The figures for countries such as Italy and Spain may also be underreported, leading to questions about the accuracy of the survey’s data in reflecting true reading habits. Nonetheless, the survey indicates that a large portion of the population is not engaging with books, making it essential to invest in more comprehensive and reliable reading surveys across Europe.

Book price increases and inflation

Over the past two decades, general inflation in Europe has increased by 64%, while book prices have only risen by 38%. This gap between general inflation and book price increases has caused concern among publishers, who fear that raising prices could make books less accessible to the public. In 2023, book prices increased by 4%, which was lower than the 6% inflation rate. In 2024, book prices finally saw an increase that roughly mirrored the general inflation rate. Despite this, publishers are still cautious about price hikes, given the risk of alienating readers or losing market share.

2024 market overview: growth and regional variations

The overall book market in 2024 is projected to grow by 2.2%, driven mainly by price increases rather than a significant rise in volumes. Notably, there are variations in performance across different regions. Spain and Portugal stand out as exceptions, with Spain experiencing consistent growth over the past decade, and Portugal recovering strongly post-COVID. In contrast, countries like Finland are showing slight negative trends, particularly in physical book sales, with growth largely coming from digital formats. The Nordic countries, while performing well in terms of market share, have seen much of their growth driven by the audio book sector and digital subscriptions, making it harder to measure their exact market impact.

Physical bookstore sales are gradually recovering in Western European markets, although the trend is less pronounced in the Nordics, where digital formats dominate. Online book sales continue to thrive, especially in countries like Sweden, Germany, Austria, and Portugal, with notable declines in traditional physical store sales in countries like Italy and the UK. This pattern reflects a broader shift toward digital purchasing channels accelerated by the pandemic.

Audiobooks and digital growth

Audiobooks have experienced significant growth, particularly in countries like Finland, Italy, Sweden, and the UK. In Finland, for example, the audiobook market has grown more than 200% in the last five years, with similar surges seen in Sweden and the UK. However, measuring the true market share of audiobooks remains challenging due to the prevalence of subscription-based services like Spotify, which makes it difficult to track actual sales or consumption patterns. In the Nordic countries, the audio format has become a dominant force, with more than **90% of growth** attributed to audio, primarily through digital subscriptions.

The Spanish phenomenon: a 10-Year growth streak

Spain presents a unique case, being the only European market on a «10-year growth streak» in book sales, continuing into 2024 with another year of growth. This remarkable consistency sets Spain apart from other European countries, where recovery has been slower. The steady growth in Spain is likely driven by a combination of factors, including a strong domestic market, educational publishing, and increased interest in both digital and print formats.

Despite this positive trend, Spain’s continued growth is also attributed to structural factors, such as its highly decentralized education system, which requires multiple editions of books in different regions, further driving the number of titles in the market. Moreover, Spain’s proximity to Latin America provides a significant export opportunity for Spanish-language books, expanding the market further.

The German market: slow recovery and digital shift

Germany, traditionally one of the largest book markets in Europe, experienced a slower recovery from the COVID-19 pandemic compared to other countries. However, by 2024, Germany has seen its market surpass pre-COVID levels, though growth remains modest at 2.4% over the past five years. This rate of recovery has not kept pace with inflation, highlighting the challenge faced by publishers in balancing price increases with consumer expectations. Like many other markets, the German book industry has seen growth in digital sales, particularly audiobooks, which continue to thrive.

2024 performance across Europe: trends and projections

Looking at the broader picture for 2024, most markets show stability, with some regional disparities in performance. In Italy, Germany, and France, the market remains relatively stable, while countries like Finland and Sweden continue to see digital-driven growth, especially in audiobooks. The UK is also seeing steady progress, with digital formats gaining ground alongside traditional print sales.

In Portugal and Spain, recovery continues to outpace other European countries, fuelled by a combination of post-COVID rebound and strong domestic and export-driven growth. The shift to digital channels is particularly notable in these regions, with online sales continuing to rise.

Key takeaways from Turrin’s presentation:

- The importance of online book purchases continues to drive the market, with a notable increase in the adoption of audiobooks and digital formats, particularly in the Nordic countries.

- Eurostat’s survey on reading habits highlights concerning trends, particularly among men, and calls for more detailed and accurate surveys to better understand reading behaviour.

- The gap between general inflation and book price increases remains a challenge for publishers, who must carefully balance accessibility with profitability.

- There are big regional differences. pain’s consistent growth over the past decade and the digital shift in the Nordic countries highlight the diverse dynamics within European book markets. The German market’s slow recovery and the positive performance of Portugal further illustrate the range of experiences across Europe.

You can follow the workshop by Enrico Turrin in this video that is incorporated also to the ThinkPub Library of Digital Learning Objects.